Key Insights into the UK Online Casino Games Market

The online casino games market is undergoing dynamic growth, distinguished not only by impressive financial performance but also by an expanding diversity of games and continuous technological innovations.

Slots, the undisputed leader, have dominated revenues and turnover for years, while traditional categories such as blackjack and roulette are struggling with declining popularity.

The analysis in this article is based on data provided by the Gambling Commission in November 2024 and focuses on key insights and trends within the UK online casino games market.

Key Takeaways

- The UK online casino market is a central part of the global online casino games market, achieving turnover of £106 billion in 2023/2024, driven by technological innovation and evolving player preferences.

- Between 2015 and 2024, gross gambling yield (GGY) in online casinos increased by 84%, from £2.4 billion to £4.4 billion, highlighting the sector’s rapid expansion and revenue-generating potential.

- Slots remain the dominant category in the UK online casino games market, accounting for 82% of gross gambling yield (GGY) and showcasing the highest efficiency in generating revenues among all game categories.

- While sports betting turnover grew modestly by 5% between 2015/2016 and 2023/2024, bingo turnover declined by 33%, despite a 37% rise in GGY, indicating a shift towards more engaged but smaller player bases.

General Data on the UK Online Casino Games Market

The online casino games market, especially in the United Kingdom, has been growing dynamically for years, as evidenced by steadily increasing turnover and gross gambling yield (GGY).

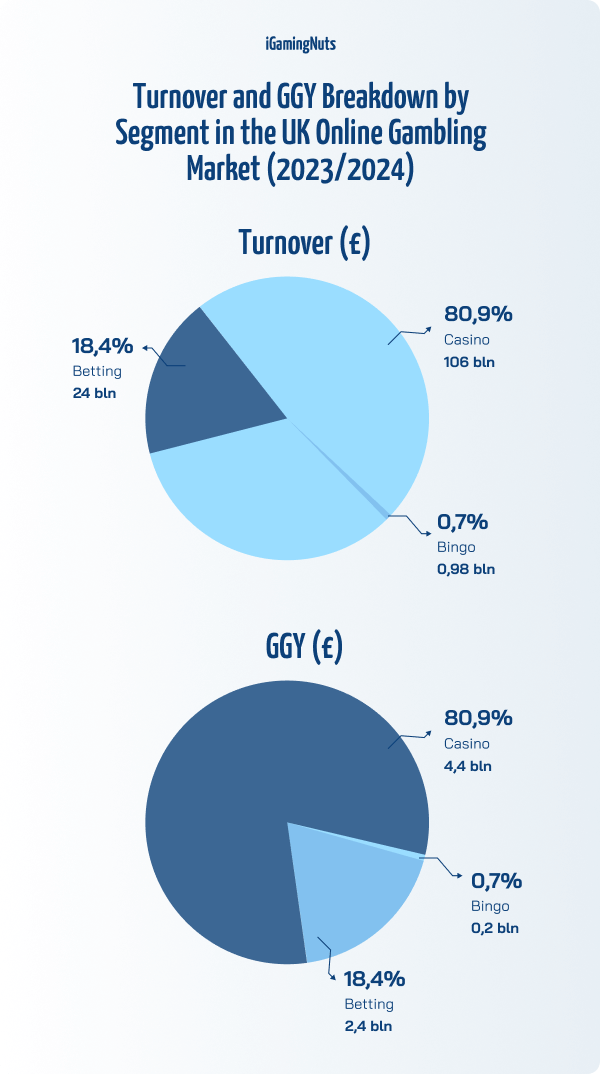

In 2023/2024, online casinos generated as much as 81% of the total turnover, while sports betting accounted for 18.5%, and bingo a mere 0.75%.

A similar dominance of online casinos is evident in the data on gross gambling yield. The share of online casinos in total GGY amounted to 63%, surpassing sports betting with 34%, and bingo, which generated just under 3%.

Development of the Online Casino Games Market: 2015–2024

Historical data analysis reveals key changes in the UK online casino games market and the broader online gambling sector over the past nine years. Online casinos have seen the most dynamic growth, but differences are also visible in the performance of sports betting and the bingo segment.

Online Casinos

In 2015/2016, turnover in online casinos was £62.3 billion, which rose to £106 billion by 2023/2024, representing a 70% increase. Even more impressive growth was observed in GGY, which increased by 84% from £2.4 billion to £4.4 billion.

These figures highlight not only the scale of growth in the online casino sector but also its ability to generate substantial revenue despite high RTP (Return to Player) rates, which increase players’ chances of winning.

Sports Betting

This segment saw turnover rise from £22.95 billion in 2015/2016 to £24.12 billion in 2023/2024, translating to a modest growth of 5%. However, more noticeable changes can be seen in GGY, which increased by 36% from £1.74 billion to £2.37 billion.

The stability of sports betting stems from player loyalty and the predictability of business models, although its growth rate is significantly lower compared to online casinos.

Bingo

The bingo segment experienced a 33% drop in turnover from £1.47 billion to £0.98 billion, indicating declining interest in this form of gambling. Nonetheless, GGY rose by 37%, from £122 million to £167 million. This increase in gross revenue may suggest that although the player base is smaller, it is more engaged, potentially reflecting a tailored offering for loyal users.

Online Casino Games – Which Categories Dominate the Market?

Online casinos offer a wide range of games, differing in both rules and player popularity. Data published by the Gambling Commission in November 2024 provides a detailed analysis of which game categories generate the highest GGY and turnover and evaluates their profitability.

Slots – The UK Market Leader

Slots have been the most popular choice among players for years, dominating the online casino games market in the UK in terms of revenues and turnover, and maintaining their position as a key driver of growth in the sector. According to market data,UK slots sites continue to dominate both player activity and operator revenues.

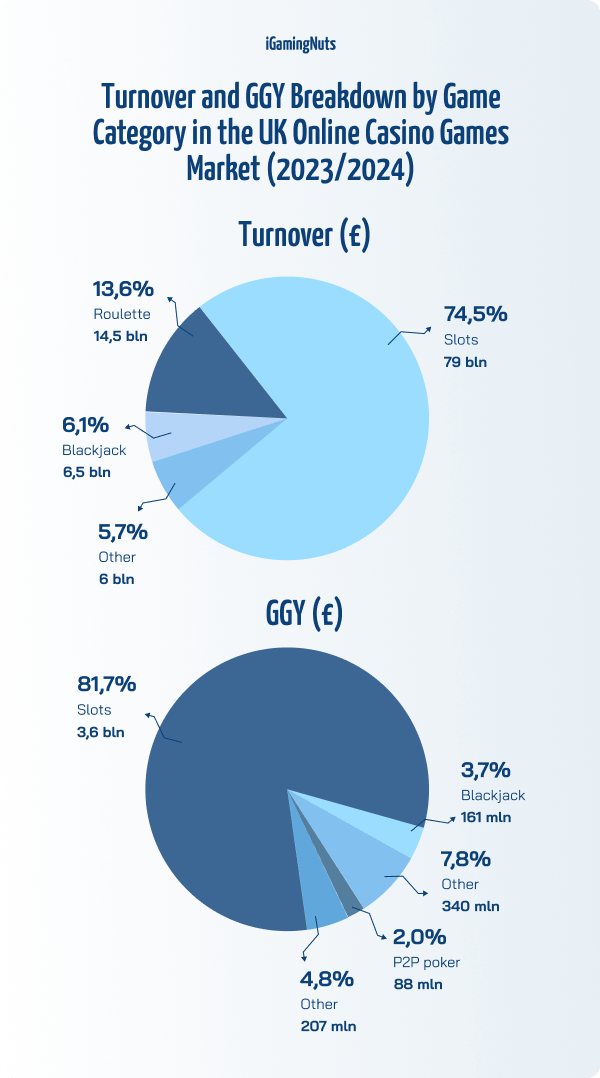

In the analysed period, they accounted for nearly 82% of total GGY, translating to gross revenues of £3.6 billion. Simultaneously, they represented 74.5% of total turnover, amounting to £79 billion.

The efficiency of slots in generating revenue is confirmed by a GGY/Turnover ratio of 4.5%, the highest among all categories analysed. This demonstrates that slots are not only the most popular but also the most profitable category for casino operators.

Why Do Slots Dominate?

- Thematic Variety: Slots offer hundreds of unique themes, ranging from mythology to contemporary pop culture.

- Modern Technologies: Advanced graphics, 3D animations, and interactive bonuses enhance the appeal of the games.

- High RTP (Return to Player): Rates of 96–98% attract players by offering them better chances of winning.

Blackjack – A Classic Game, But Is It Still Attractive?

Blackjack, one of the most classic casino games, records a relatively low share in revenues and turnover. In 2023/2024, it accounted for 3.7% of GGY (£161 million) and 6% of turnover (£6.5 billion). Its GGY/Turnover ratio of 2.5% makes it one of the less efficient categories. Nevertheless, free online blackjack variants remain popular for practice and recreational play.

Why Is Blackjack Losing Ground?

- Lack of Innovation: Compared to more dynamic categories, blackjack offers limited diversity.

- Competition from Slots: Dynamic, interactive slots attract a larger number of players, especially younger ones.

Roulette: An Iconic Game Facing Future Challenges

Roulette ranks third in market share, generating nearly 8% of GGY (£340 million) and 13.7% of turnover (£14.5 billion). However, its GGY/Turnover ratio of 2.4% indicates low efficiency in generating revenue from turnover. Despite this, online roulette continues to attract players interested in live formats and strategic variations.

Factors Influencing Roulette’s Popularity:

- Live Roulette Popularity: Live-format games attract players looking for experiences similar to land-based casinos.

- Traditional Nature of the Game: Roulette appeals to loyal players but does not always meet the needs of new users.

Peer-to-Peer Poker – Stability in a Niche

Peer-to-Peer Poker remains a niche category, generating only 2% of GGY (£88 million). The lack of turnover data prevents a precise assessment of this category’s efficiency, but its marginal role compared to market leaders is evident.

Development Opportunities for Peer-to-Peer Poker:

- Introduction of new tournament formats.

- Integration with social media, potentially attracting younger players.

Other Games – A Stable Element of the Offering

The “Other” category encompasses a wide range of games that collectively account for 4.8% of GGY (£207 million) and 5.7% of turnover (£6 billion). A GGY/Turnover ratio of 3.4% indicates moderate efficiency in generating revenue, second only to slots.

Significance and Development Potential

- Games in this category cater to the preferences of specific player groups, making them a stable yet small market segment.

- Further investments in developing unique products could enhance their popularity and increase their market share.

During the analysed period, slots not only dominate the market but also demonstrate the highest efficiency in generating revenues. Traditional games such as blackjack and roulette still have their loyal players, but they are clearly losing ground to more dynamic and innovative categories.

Analysis of Trends Over the Years: Data, Dynamics, and Projections

In recent years, the online casino games market in the UK and globally has undergone significant changes, driven by external events such as the COVID-19 pandemic and the evolving preferences of players.

The growing popularity of mobile gaming,, advancements in technology, and a diverse range of offerings have contributed to the sector’s transformation. An analysis of trends in key categories, such as slots, blackjack, and roulette, not only helps to understand market dynamics but also highlights directions for future growth.

To better illustrate changes over the years, the analysis incorporates the Compound Annual Growth Rate (CAGR), which measures the average annual growth of a value over a specific period while accounting for the effects of compounding.

This metric provides insights into long-term trends in figures like Gross Gambling Yield (GGY) and market share, smoothing out short-term fluctuations.

Slots in the UK Online Casino Games Market

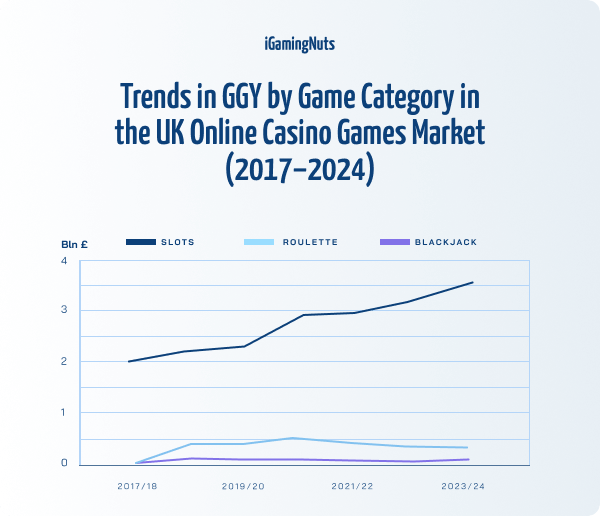

Slots have dominated the online casino segment for years, steadily increasing their share of GGY. In 2015/2016, this category accounted for 66% of total GGY, which rose to an impressive 82% in 2023/2024. An analysis of CAGR highlights three key periods of growth.

Trends Over the Years

- 2015–2020: Stable growth with an average annual increase of 8.5%, driven by the rising popularity of online gaming and investments in new features and technologies.

- 2020–2021: A sharp increase of 24.5% during the COVID-19 pandemic, when interest in online entertainment peaked.

- 2021–2024: Following a period of rapid growth, the slots market stabilised with an average annual growth rate of 6.8%, reflecting the maturity of this category and its established market position.

The dominance of slots in online casino revenue and turnover stems from their ability to combine visual appeal with intuitive gameplay. Thematic variety, advanced technologies such as 3D graphics and interactive bonuses, and high Return to Player (RTP) rates make slots not only popular among players but also the most profitable for operators.

These characteristics, along with easy access via mobile devices, ensure that this category remains the cornerstone of the online casino games market in the UK.

Blackjack: Peaks and Troughs

Blackjack, one of the most classic table games, has exhibited significant variability in performance over recent years. Between 2017 and 2020, the game experienced dynamic growth with a CAGR of 55.4%, attributed to increased interest in traditional casino games.

In 2020, the growth rate slowed to a moderate 5.3% as players shifted their activities online during the pandemic. However, from 2021 to 2024, blackjack’s popularity declined, with a negative CAGR of −6.2%, signalling waning interest in the category.

Market Share

Blackjack’s share of GGY peaked at 6.9% in 2018/2019 but fell to 3.7% in 2023/2024. This trend highlights the game’s declining relevance in the online casino market.

The decline in blackjack’s popularity is primarily due to a lack of innovation and intense competition from more dynamic categories, such as slots. To reverse this trend, operators must consider modernising blackjack by introducing new game variants and incorporating interactive and gamified elements that could attract younger generations of players.

Roulette: Challenges and Successes

Roulette, regarded as one of the most iconic casino games, has experienced fluctuating popularity. Between 2018 and 2020, it recorded a slight decline with a CAGR of − 0.6%, indicating some stabilisation in interest.

From 2020 to 2021, during the pandemic, roulette saw a significant increase in popularity, with a remarkable CAGR of nearly 23%, driven by the success of live games replicating the experience of land-based casinos. However, from 2021 to 2024, roulette faced declining interest, with a negative CAGR of −14%.

Market Share

Roulette’s share of GGY fell from 14% in 2018/2019 to 7.8% in 2023/2024. While the game retains a loyal player base, its overall market share continues to diminish, raising concerns for casino operators.

Despite the temporary resurgence during the pandemic, roulette faces challenges in attracting and retaining players. To reverse this trend, further innovations, such as live roulette enhancements and gamification elements, could make the game more dynamic and appealing to new users.

Key Insights from Trends

- Slots will continue to dominate the market due to their high efficiency in generating revenues (GGY/Turnover of 4.5%) and consistent growth.

- Blackjack requires modernisation to regain its former popularity.

- Roulette faces the challenge of adapting to new player expectations, which may require substantial investment in live online formats.

- The pandemic played a pivotal role in shaping market trends, but the market is stabilising post-pandemic, with evident growth for the most dynamic and innovative games.

What Lies Ahead for the Online Casino Market?

The online casino games market is evolving rapidly, with trends like the dominance of slots and the decline of traditional table games shaping its future. Insights from the UK market highlight opportunities for innovation and adaptation. Understanding these shifts is key to staying competitive in this dynamic industry.

1. Dominance of Slots – A Continuing Trend

Slots have long maintained their position as the leading category in online casinos, and historical data confirms their consistent growth. Despite market stabilisation between 2021 and 2024, with a CAGR of 6.8%, slots continue to generate the largest share of both gross gambling yield and turnover.

Forecasts indicate that slots will remain dominant due to their flexibility and capacity to adapt to new technologies. Innovations such as virtual reality (VR) and advanced 3D graphics are expected to attract new players, while personalised experiences powered by artificial intelligence will increase engagement among existing users.

Additionally, the widespread availability of mobile slots allows players to access games anytime, anywhere, further driving their growth.

2. Decline in Popularity of Blackjack and Roulette

Historical data shows that traditional table games, such as blackjack and roulette, are losing ground in the online gaming market. Between 2021 and 2024, blackjack experienced a CAGR decline of -6.2%, with its share of gross gambling yield decreasing to 3.7%.

Similarly, roulette saw a CAGR of -14% during the same period, with its GGY share falling from 14% in 2018/2019 to 7.8% in 2023/2024.

The decline is primarily attributed to intense competition from more dynamic and innovative categories like slots. To reverse this trend, operators should consider modernising blackjack and roulette by introducing new game variants, gamification elements, and enhancing live formats, which appeal to players seeking experiences akin to traditional casinos.

3. Stability of Niche Categories

Niche categories such as Peer-to-Peer Poker and “Other” games maintain a stable position in the market. Peer-to-Peer Poker, despite accounting for only 2% of GGY, benefits from a loyal player base.

Meanwhile, the “Other” games category has seen moderate growth, contributing nearly 5% to GGY. The stability of these segments is rooted in their tailored offerings, which cater to specific player groups.

To increase market share, operators could focus on introducing innovations such as new tournament formats or integrating games with social media platforms, which may attract younger generations of players.

4. Technology and Regulations as Key Development Drivers

Technological advancements and regulations promoting responsible gambling will significantly shape the market’s future. Artificial intelligence (AI) will enable operators to provide more personalised player experiences, while the adoption of virtual reality (VR) may unlock new opportunities for immersive game formats.

At the same time, stricter regulations aimed at player protection and responsible gambling will compel operators to refine their marketing and bonus strategies. Balancing market growth with player safety will be critical to fostering a sustainable and positive industry reputation.

Future Projections

Based on current trends, slots are expected to continue their growth and dominance in GGY, while blackjack and roulette will require substantial modernisation efforts to stem their declines. By leveraging emerging technologies and adhering to regulatory demands, the online casino market is poised to expand while adapting to evolving player preferences and industry standards.

Differences Between Turnover and Gross Gambling Yield: Market Specifics Explained

Turnover refers to the total amount wagered by players, while Gross Gambling Yield (GGY) represents the funds retained by operators after paying out winnings. These two metrics vary significantly depending on the nature of the games and operators’ strategies, influencing how profitability is interpreted and assessed.

Online Casinos Specifics

During the analysed period (2023–2024), online casinos generated a turnover of £106 billion, with a GGY of £4.4 billion. The GGY/Turnover ratio of 4% highlights that operators retain only a small portion of the total amount wagered.

- High RTP (Return to Player)

Casino games, especially slots, are characterised by high RTP rates, often ranging between 96% and 98%. This means the majority of wagered funds are returned to players as winnings, leaving operators with relatively low margins.

Example: Slots

- Turnover: £79 billion

- GGY: £3.6 billion

- GGY/Turnover Ratio: 4.5%

Slots generate high turnover, but their profitability is constrained by high RTPs, which increase players’ chances of winning.

Sports Betting Specifics

Sports betting during the same period achieved a turnover of £24 billion, with a GGY of £2.4 billion. The GGY/Turnover ratio of 9.8% is more than double that of online casinos, reflecting greater efficiency in generating profits.

- Lower RTP and Higher Margins

Sports betting typically offers lower RTP rates, usually between 85% and 90%. Reduced payouts to players allow operators to retain a larger share of the stakes.

Example: Sports Betting

- Turnover: £24 billion

- GGY: £2.4 billion

- GGY/Turnover Ratio: 9.8%

While sports betting generates lower turnover compared to casinos, it achieves higher margins, making it more profitable relative to the amount wagered.

Key Differences Between GGY and Turnover

These differences reflect the nature of the games and operators’ strategies. Online casinos attract high turnover due to the popularity of high-RTP games, but their revenue generation efficiency remains low. In contrast, sports betting, while less popular in terms of turnover, achieves higher margins, making it more profitable per unit wagered.

Trends and Future of the UK Online Casino Games Market

The online casino market leads the dynamic gambling sector, distinguished by its growing diversity of games and ongoing technological innovations. An analysis of the past nine years shows that slots not only dominate in terms of revenue and turnover but also set benchmarks for efficiency in generating profits.

Their popularity stems from the combination of modern technologies, intuitive gameplay, and attractive RTP rates, ensuring high player satisfaction.

Traditional games, such as blackjack and roulette, face the challenge of adapting to shifting player preferences. The declining popularity of these categories highlights the need for innovation to make them more dynamic and interactive. Meanwhile, niche segments like Peer-to-Peer Poker remain stable, relying on a loyal player base.

Looking ahead, key drivers for market development will include technological innovations such as artificial intelligence and virtual reality, which have the potential to revolutionise player experiences. At the same time, stricter regulations on responsible gambling will compel operators to balance growth with player protection.

These insights demonstrate that the UK online casino games market is not only a leader in the gambling industry but also a key indicator of how the broader online casino games market is evolving globally – flexibly adapting to new technologies, changing player needs, and regulatory demands.